Dept Warehousing

We previously informed you of the availability to warehouse your tax debts associated with COVID-19. We outlined the following:

- The eligibility to warehouse COVID debts,

- The taxes which could be warehoused,

- How long the tax debts could be warehoused, and

- The interest rates that would apply to the warehoused debts.

To review our previous correspondence, please click the following links:

Warehouse VAT and PAYE Employer Tax Debts dated 19th June 2020.

Warehouse Income Tax Debts dated 23rd October 2020.

This circular deals with VAT and PAYE.

Arrangements to repay the warehoused debts:

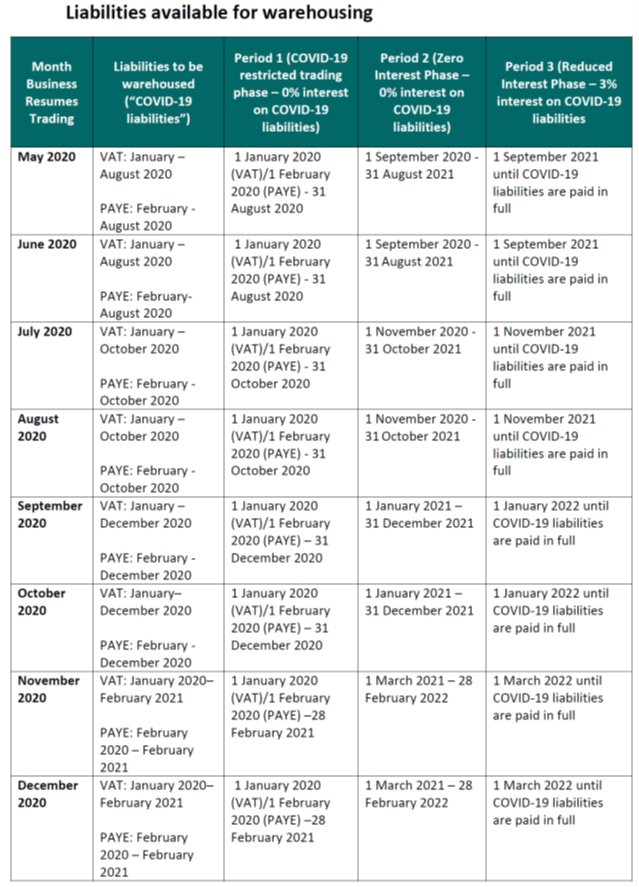

Taxpayers who have warehoused tax debts should contact Revenue to put arrangements in place to repay the warehoused debts before the end of the 0% interest rate period. The end of the 0% interest rate period will depend on when your business resumed trading but should not be earlier than 31 August 2021. See below for a schedule of when the 0% ceases.

For example:

Joe’s business closed in March 2020 due to COVID. He commenced to trade again in June 2020.

Joe was entitled to warehouse the following liabilities:

- VAT from January to August 2020

- PAYE/PRSI from February to August 2020.

The 0% interest rate on the above debts apply up to 31 August 2021 (3% interest thereafter).

Joe should contact Revenue to set up a Phased Payment Arrangement (PPA) to repay the warehoused debt before 31 August 2021.

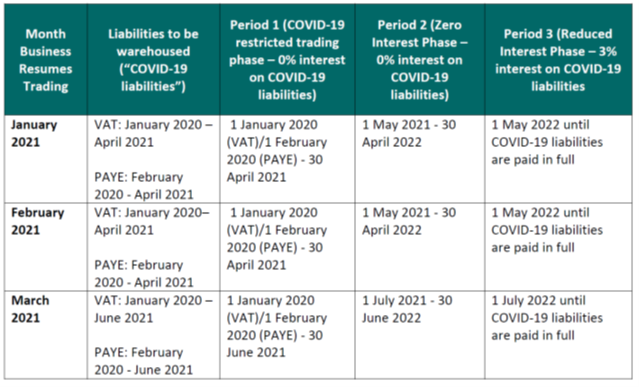

What if Joe’s business had to close again in December 2020 due to the re-imposition of COVID restrictions?

In this instance Joe can avail of extended warehousing periods for his tax debts.

On the assumption that Joe re-opens before the end of February 2021, he would be entitled to warehouse the following liabilities:

- VAT from January 2020 to April 2021

- PAYE/PRSI from February 2020 to April 2021.

The 0% interest rate will apply up to April 2022 (3% interest thereafter).

Please note that VAT and/or PAYE/PRSI returns already submitted to Revenue and where the liabilities have been paid will not qualify for warehousing.

Joe should contact Revenue to set up a Phased Payment Arrangement (PPA) to repay the warehoused debt before 30 April 2022.

Phased payment arrangement:

We would advise early and meaningful engagement with Revenue to agree payment arrangements that are acceptable to both yourself and Revenue.

Applications for Phased Payment Arrangements (PPA) can be made online through Revenue Online Services (ROS).

The duration of the phased payment required will vary dependant on individual taxpayer circumstances. This can be set out by the applicant when the phased payment application is being made. The duration required will be reviewed by Revenue on a case-by-case basis and the taxpayer will be advised accordingly. This online facility is available 24/7 and affords businesses considerable flexibility to self-manage their tax payment schedule in line with business needs or temporary cash flow challenges.

For those businesses that have no capacity at present to pay their current taxes or meet the PPA obligations, the taxpayer may defer the PPA payment by one month via the online facility. Alternatively, a taxpayer may seek a deferral in excess of one month and such requests will be considered on a case-by-case basis.

While significant down payments are generally demanded by Revenue, there is flexibility in this regard in these times of Covid-19.

If you wish to discuss further, please contact either Francis Moriarty, Kevin Bambury or your usual PSC contact.